The Petro Government by the Numbers (1/3): An Economic Balance of Colombia's First Progressive Government

Ahead of the 2026 presidential election in Colombia, it is worth taking a brief, impartial look at the results of the country's first progressive government. The goal is to assess, based on facts rather than political passion, how the government did on the economy, welfare and security. In this first part, we focus only on economic performance.

June 19, 2022 was a date for the history books: for the first time in Colombia, a candidate from the so-called “progressive” movement reached the presidency. In a very tight race against right-wing candidate Rodolfo Hernández (50.44% to 47.31%), Gustavo Petro prevailed at the polls and succeeded Iván Duque in the Casa de Nariño. With an ambitious program, he won the votes of more than 11 million Colombians.

Now, as the term draws to a close, it is possible to make a preliminary assessment of some of the most notable results of the Petro government and of the political project that today hopes to win the 2026 presidential election once again. To do so, we will take a broad look at its economic performance based on the available data.

It is worth noting that not every improvement in an indicator necessarily means the country is better off. A figure can improve for worrying reasons. Crime can fall not because of a stronger state presence, but because criminal groups control certain territories; or unemployment can drop not because there are more job opportunities, but because many people stop looking for work. That is why, beyond the result, it is key to look at the causes and their effects — because that is usually where long-term structural problems arise.

Economic performance: stabilization, stagnation and fiscal challenges

The economic front during the 2022-2026 period has been marked by an attempt to shift toward a model driven by state spending and redistribution, which has produced highly asymmetric results across sectors, a stagnation of real productivity, and unprecedented pressure on public finances.

GDP growth and the exhaustion of private investment

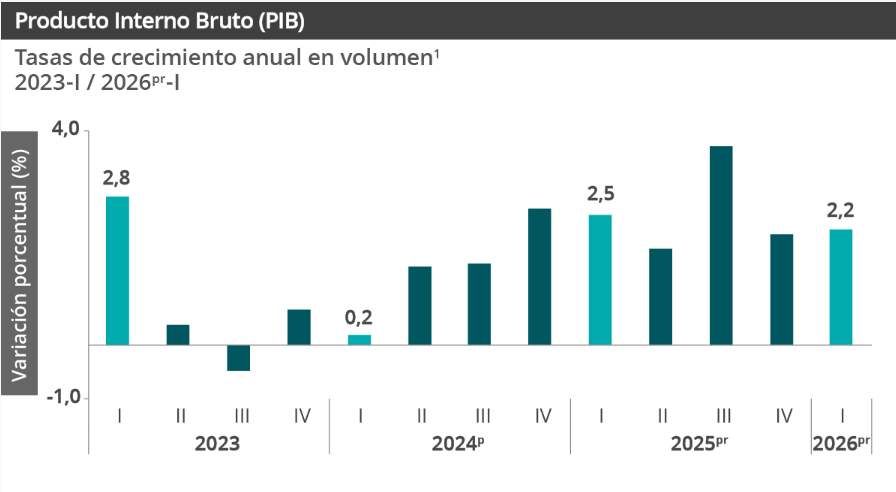

After the strong economic rebound Colombia experienced following the pandemic, when GDP grew 7.3% in 2022, the economy lost steam in 2023 and grew just 0.6%. In the following years, however, it began to show a gradual recovery: it grew 1.7% in 2024, reached 2.6% in 2025, and, during the first quarter of 2026, posted year-over-year growth of 2.2%.

Even so, when you look more closely at where that growth comes from, warning signs appear. Much of the expansion seems concentrated in sectors such as public administration and defense — closely tied to state spending — and in entertainment activities. By contrast, sectors that are key to production and exports, such as manufacturing and mining, have performed weakly or even negatively. On top of this, business investment fell sharply, dropping to 16% of GDP, its lowest level in two decades.

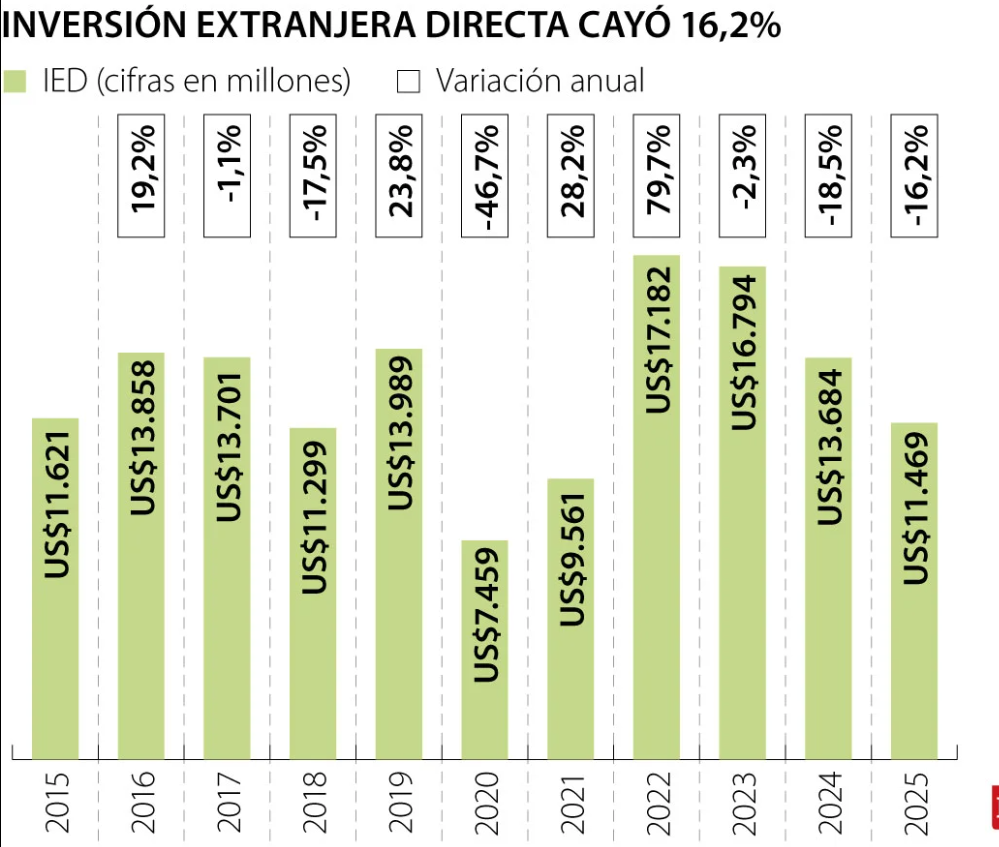

The Collapse of Foreign Direct Investment (FDI)

Regulatory uncertainty in Colombia has begun to show up more clearly in investment decisions. For the first quarter of 2026, Foreign Direct Investment reached US$2.129 billion, a 9.1% drop versus the same period the previous year and one of the weakest starts to a year in the last five.

A clear example of this is the mining and energy sector. The government’s decision not to sign new hydrocarbon exploration contracts reduced the interest of several investors in a sector that has historically carried significant weight within the foreign investment that reaches the country. In addition, various statements that threatened to tax international transfers were received with displeasure by the foreign community.

While boosting sectors such as agriculture and tourism is a desirable bet to diversify the economy, so far it has not been enough to offset the income Colombia has traditionally received from hydrocarbons. The result has been greater pressure on the government’s finances and a fiscal deficit that is causing increasing concern.

Fiscal sustainability: stagnant revenue and runaway spending

The fiscal front has become one of Colombia’s main concerns. While the government’s revenue has weakened, public spending has continued to grow, especially through larger transfers for health, pensions and social subsidies. This pressure pushed the fiscal deficit to levels close to the limit allowed by the Fiscal Rule and contributed to S&P Global Ratings downgrading the country’s sovereign rating to BB-.

So the government is collecting less and spending more. It is a situation that, even in our personal finances, we would hardly accept: if we spend more than we earn, sooner or later we will have to borrow. And when debt grows too much, it ends up compromising future income and reducing room to maneuver in the cash account.

We cannot set inflation aside, which fell from a critical 13.1% in 2022 to stabilize around 5.1% at the close of 2025. However, on an explicit regional comparison, Colombia shows a marked inflation lag against its peers in April 2026: Brazil posted 4.39%, Mexico 4.45%, and Peru held at a stable 4.0%.

The economic balance of the first progressive government: stabilization of inflation and the peso, but at the cost of a fiscal deficit that cost Colombia its investment-grade rating.

Now, at first glance it might seem that the exchange-rate situation works in the country’s favor: the Colombian peso has strengthened against the dollar and the exchange rate has stayed at lower levels than in recent years. But a stronger currency does not necessarily mean the economy is free of risk. The minimum-wage increase, together with increasingly expensive public debt, may keep pressuring the government’s finances. On one hand, higher labor costs end up affecting various state expenses; on the other, interest payments reduce the resources available for social investment, infrastructure and future growth.

Conclusions

The first thing to say — because it is obvious — is that many of the dire predictions about Colombia did not come true. We did not become a “second Venezuela,” the dollar did not reach $10,000 pesos, and the economy did not collapse as some announced in apocalyptic tones. So perhaps this is a good opportunity to look beyond the scare and focus on what matters: the ideas, the results and their consequences.

On the economy, these four years were marked by a clear bet: a more active state, more public spending, and a far more ambitious social program. The problem is that this bet also came at a cost. The government tried to expand social investment and deliver on a fairly large agenda, but along the way it ended up pressuring public finances. With a strong opposition in Congress and a growing need for resources, the country ended up resorting to more expensive debt and committing part of its future income.

Now, this should not surprise us too much. Progressivism, by definition, tends to defend a stronger role for the state in the economy. Whether that is good or bad is an enormous debate, one that has gone on for decades and that I do not intend to resolve in this article — not even with three cups of coffee and a whole free Sunday. What does seem clear is that, under governments like Petro’s, or eventually under leadership like Iván Cepeda’s, the state would tend to take an ever-larger presence in the economy.

And no, this does not necessarily mean Colombia will nationalize everything or that tomorrow we will wake up standing in line to buy bread. But it does imply a direction: more state intervention, more public spending, and more faith that the government can better steer certain sectors of the economy. In my judgment, that is where the main risk lies. Not because all state intervention is bad, but because when the state plays God, it stops correcting market failures and starts manufacturing them, handing out privileges where there used to be competition and centralizing power to the detriment of democracy.